Buying

a put option

A put

option (sometimes simply called a "put") is a financial

contract between two parties, the buyer and the writer (seller)

of the option. The put allows the buyer the right but not

the obligation to sell a commodity or financial instrument

(the underlying instrument) to the writer (seller) of the option

at a certain time for a certain price (the strike price). The

writer (seller) has the obligation to purchase the underlying

asset at that strike price, if the buyer exercises the option.

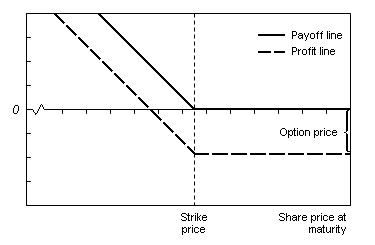

This

is a graphical interpretation of the payoffs and profits

generated by a put option as seen by the buyer

of the option. A lower stock price means a higher

profit.

Eventually, the price of the underlying security will

be low enough to fully compensate for the price of

the option.

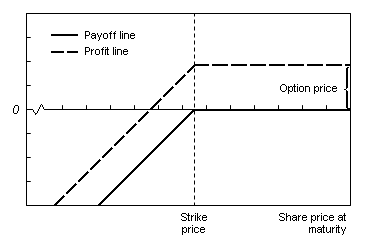

Writing

a put option - This is a graphical interpretation

of the payoffs and profits generated by a put

option as seen by the writer of the option. Profit

is maximized when the price of the underlying security

exceeds the strike price, because the option expires

worthless and the writer keeps the premium.

Note that

the writer of the option is agreeing to buy the underlying

asset if the buyer exercises the option. In exchange for having

this option, the buyer pays the writer (seller) a fee (the premium).

(Note: Although option writers are frequently referred to as

sellers, because they initially sell the option that they create,

thus taking a long position in the option, they are not the

only sellers. An option holder can also sell his short position

in the option. However, the difference between the two sellers

is that the option writer takes on the legal obligation to buy

the underlying asset at the strike price, whereas the option

holder is merely selling his short position, and is not contractually

obligated by the sold option.)

Exact specifications

may differ depending on option style. A European put option

allows the holder to exercise the put option for a short period

of time right before expiration. An American put option allows

exercise at any time during the life of the option.

The most

widely-known put option is for stock in a particular company.

However, options are traded on many other assets: financial

- such as interest rates (see interest rate floor) - and physical,

such as gold or crude oil.

The put

buyer either believes it's likely the price of the underlying

asset will fall by the exercise date, or hopes to protect a

long position in the asset. The advantage of buying a put over

shorting the asset is that the risk is limited to the premium.

The put writer does not believe the price of the underlying

security is likely to fall. The writer sells the put to collect

the premium. Puts can also be used to limit portfolio risk,

and may be part of an option spread.

Example

of a put option on a stock

Buy a Put: Ty Eriksen thinks price of a stock will decrease.

Pay a premium which buyer will never get back.

The buyer has the right to sell the stock

at strike price.

Write a put: Writer receives a premium.

If buyer exercises the option,

writer will buy the stock at strike price.

If buyer does not exercise the option,

writer's profit is premium.

- 'Trader

A' (Put Buyer) purchases a put contract to sell 100

shares of XYZ Corp. to 'Trader B' (Put Writer) for

$50/share. The current price is $55/share,

and 'Trader A' pays a premium of $5/share. If the

price of XYZ stock falls to 40/share right before

expiration, then 'Trader A' can exercise the put by buying

100 shares for $4,000 from the stock market, then selling

them to 'Trader B' for $5,000.

Trader A's total earnings (S) can be calculated at $500.

Sale of the 100 stock at strike price of $50 to 'Trader B' = $5,000 (P)

Purchase of 100 stock at $40 = $4,000 (Q)

Put Option premium paid to Trader B for buying the contract of 100 shares @ $5/share, excluding commissions = $500 (R)

S=P-(Q+R)=$5,000-($4,000+$500)=$500

- If, however,

the share price never drops below the strike price (in this

case, $50), then 'Trader A' would not exercise the option.

(Why sell a stock to 'Trader B' at $50, if it would cost 'Trader

A' more than that to buy it?). Trader A's option would be

worthless and he would have lost the whole investment, the

fee (premium) for the option contract, $500 (5/share,

100 shares per contract). Trader A's total loss are limited

to the cost of the put premium plus the sales commission to

buy it.

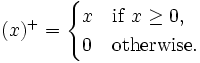

This example illustrates that the put option has positive monetary

value when the underlying instrument has a spot price (S)

below the strike price (K). Since the option will

not be exercised unless it is "in-the-money", the payoff for

a put option is

- max[(K ŌłÆ S) ;

0] or formally, (K ŌłÆ S) +

- where :

Prior to

exercise, the option value, and therefore price, varies with

the underlying price and with time. The put price must reflect

the "likelihood" or chance of the option "finishing in-the-money".

The price should thus be higher with more time to expiry, and

with a more volatile underlying

instrument. The science of determining this value is the central

tenet of financial mathematics. The most common method is to

use the Black-Scholes formula. Whatever the formula used, the

buyer and seller must agree on this value initially.

See

also

External

links