An

interest rate swap is a derivative in which one party exchanges a stream

of interest payments for another party's stream of cash flows.

Interest rate swaps can be used by hedgers to manage their fixed

or floating assets and liabilities. They can also be used by

speculators to replicate unfunded bond exposures to profit from

changes in interest rates. As such, interest rate swaps are

very popular and highly liquid instruments.

Structure

In an interest

rate swap, each counterparty agrees to pay either a fixed or

floating rate denominated in a particular currency to the other

counterparty. The fixed or floating rate is multiplied by a

notional principal amount (say, USD 1 million). This notional

amount is generally not exchanged between counterparties, but

is used only for calculating the size of cashflows to be exchanged.

The most

common interest rate swap is one where one counterparty pays

a fixed rate (the swap rate) while receiving a floating rate

(usually pegged to LIBOR). Consider the following swap in which

Party A agrees to pay Party B periodic interest rate payments

of LIBOR + 50 bps (0.50%) in exchange for periodic interest

rate payments of 3.00%. Note that there is no exchange of the

principal amounts and that the interest rates are on a "notional"

(i.e. imaginary) principal amount. Also note that the interest

payments are settled in net (e.g. if LIBOR + 50 bps is 1.20%

then Party A receives 1.80% and Party B pays 1.80%). The fixed

rate (3.00% in this example) is referred to as the swap rate.[1]

At the point

of initiation of the swap, the swap is priced so that it has

a net present value of zero. If one party wants to pay 50 bps

above the par swap rate, the other party has to pay approximately

50 bps over LIBOR to compensate for this.

Types

Being OTC

instruments interest rate swaps can come in a huge number of

varieties and can be structured to meet the specific needs of

the counterparties. That said, by far the most common are fixed-for-fixed,

fixed-for-floating or floating-for-floating. The legs of the

swap can be in the same currency or in different currencies.

(A single-currency fixed-for-fixed rate swap is generally not

possible; since the entire cash-flow stream can be predicted

at the outset there would be no reason to maintain a swap contract

as the two parties could just settle for the difference between

the present values of the two fixed streams, the only exceptions

would be where the notional amount on one leg is uncertain or

other esoteric uncertainty is introduced)

Fixed-for-floating

rate swap, same currency

Party P

pays/receives fixed interest in currency A to receive/pay floating

rate in currency A indexed to X on a notional N for a tenor

T years. For example, you pay fixed 5.32% monthly to receive

USD 1M Libor monthly on a notional USD 1 million for 3 years.

The party that pays fixed and receives floating coupon rates

is said to be long the interest swap.

Fixed-for-floating

swaps in same currency are used to convert a fixed rate asset/liability

to a floating rate asset/liability or vice versa. For example,

if a company has a fixed rate USD 10 million loan at 5.3% paid

monthly and a floating rate investment of USD 10 million that

returns USD 1M Libor +25 bps monthly, it may enter into a fixed-for-floating

swap. In this swap, the company would pay a floating USD 1M

Libor+25 bps and receive a 5.5% fixed rate, locking in 20bps

profit.

Fixed-for-floating

rate swap, different currencies

Party P

pays/receives fixed interest in currency A to receive/pay floating

rate in currency B indexed to X on a notional N at an initial

exchange rate of FX for a tenure of T years. For example, you

pay fixed 5.32% on the USD notional 10 million quarterly to

receive JPY 3M (JIBOR) monthly on a JPY notional 1.2 billion

(at an initial exchange rate of USDJPY 120) for 3 years. For

nondeliverable swaps, the USD equivalent of JPY interest will

be paid/received (according to the FX rate on the FX fixing

date for the interest payment day). No initial exchange of the

notional amount occurs unless the Fx fixing date and the swap

start date fall in the future.

Fixed-for-floating

swaps in different currencies are used to convert a fixed rate

asset/liability in one currency to a floating rate asset/liability

in a different currency, or vice versa. For example, if a company

has a fixed rate USD 10 million loan at 5.3% paid monthly and

a floating rate investment of JPY 1.2 billion that returns JPY

1M Libor +50 bps monthly, and wants to lock in the profit in

USD as they expect the JPY 1M Libor to go down or USDJPY to

go up (JPY depreciate against USD), then they may enter into

a Fixed-Floating swap in different currency where the company

pays floating JPY 1M Libor+50 bps and receives 5.6% fixed rate,

locking in 30bps profit against the interest rate and the fx

exposure.

Floating-for-floating

rate swap, same currency

Party P

pays/receives floating interest in currency A Indexed to X to

receive/pay floating rate in currency A indexed to Y on a notional

N for a tenor T years. For example, you pay JPY 1M Libor monthly

to receive JPY 1M Tibor monthly on a notional JPY 1 billion

for 3 years.

Floating-for-floating

rate swaps are used to hedge against or speculate on the spread

between the two indexes widening or narrowing. For example,

if a company has a floating rate loan at JPY 1M Libor and the

company has an investment that returns JPY 1M Tibor+30 bps and

currently the JPY 1M Tibor = JPY 1M Libor +10bps. At the moment,

this company has a net profit of 40 bps. If the company thinks

JPY 1M tibor is going to come down or JPY 1M Libor is going

to increase in the future and wants to insulate from this risk,

they can enter into a Float float swap in same currency where

they pay JPY TIBOR +10 bps and receive JPY LIBOR+35 bps. with

this, they have effectively locked in a 15 bps profit instead

of running with a current 40 bps gain and index risk. The 5bps

difference comes from the swap cost which includes the market

expectations of the future rates in these two indices and the

bid/offer spread which is the swap commission for the swap dealer.

Floating-for-floating

rate swaps are also seen where both sides reference the same

index, but on different payment dates, or use different business

day conventions. These have almost no use for speculation, but

can be vital for asset-liability management. An example would

be swapping 3M Libor being paid with prior non-business day

convention, quarterly on JAJO (i.e. Jan, Apr, Jul, Oct) 30,

into FMAN (i.e. Feb, May, Aug, Nov) 28 modified following.

Floating-for-floating

rate swap, different currencies

Party P

pays/receives floating interest in currency A indexed to X to

receive/pay floating rate in currency B indexed to Y on a notional

N at an initial exchange rate of FX for a tenor T years. For

example, you pay floating USD 1M Libor on the USD notional 10

million quarterly to receive JPY 3M Tibor monthly on a JPY notional

1.2 billion (at an initial exchange rate of USDJPY 120) for

4 years.

To explain

the use of this type of swap, consider a US company operating

in Japan. To fund their Japanese growth, they need JPY 10 billion.

The easiest option for the company is to issue debt in Japan.

As the company might be new in the Japanese market without a

well known reputation among the Japanese investors, this can

be an expensive option. Added on top of this, the company might

not have appropriate debt issuance program in Japan and they

might lack sophisticated treasury operation in Japan. To overcome

the above problems, it can issue USD debt and convert to JPY

in the FX market. Although this option solves the first problem,

it introduces two new risks to the company:

- FX risk.

If this USDJPY spot goes up at the maturity of the debt, then

when the company converts the JPY to USD to pay back its matured

debt, it receives less USD and suffers a loss.

- USD and

JPY interest rate risk. If the JPY rates come down, the return

on the investment in Japan might go down and this introduces

an interest rate risk component.

The first

exposure in the above can be hedged using long dated FX forward

contracts but this introduces a new risk where the implied rate

from the FX spot and the FX forward is a fixed rate but the

JPY investment returns a floating rate. Although there are several

alternatives to hedge both the exposures effectively without

introducing new risks, the easiest and the most cost effective

alternative would be to use a floating-for-floating swap in

different currencies. In this, the company raises USD by issuing

USD Debt and swaps it to JPY. It receives USD floating rate

(so matching the interest payments on the USD Debt) and pays

JPY floating rate matching the returns on the JPY investment.

Fixed-for-fixed

rate swap, different currencies

Party P

pays/receives fixed interest in currency A to receive/pay fixed

rate in currency B for a term of T years. For example, you pay

JPY 1.6% on a JPY notional of 1.2 billion and receive USD 5.36%

on the USD equivalent notional of 10 million at an initial exchange

rate of USDJPY 120.

Other

variations

A number

of other variations are possible, although far less common.

Mostly tweaks are made to ensure that a bond is hedged "perfectly",

so that all the interest payments received are exactly offset

by the swap. This can lead to swaps where principal is paid

on one or more legs, rather than just interest (for example

to hedge a coupon strip), or where the balance of the swap is

automatically adjusted to match that of a prepaying bond (such

as RMBS).

Uses

Interest

rate swaps were originally created to allow multi-national companies

to evade exchange controls. Today, interest rate swaps are used

to hedge against or speculate on changes in interest rates.

Hedging

Today, interest

rate swaps are often used by firms to alter their exposure to

interest-rate fluctuations, by swapping fixed-rate obligations

for floating rate obligations, or vice versa. By swapping interest

rates, a firm is able to alter its interest rate exposures and

bring them in line with management's appetite for interest rate

risk. For example, Fannie Mae uses interest rate derivatives to

hedge its cash flows. The products it uses are pay-fixed swaps,

receive-fixed swaps, basis swaps, interest rate cap and swaptions,

and forward starting swaps. Its "cash flow hedges" had a notional

value of $872 billion at December 31, 2003, while its "fair value

hedges" stood at $169 billion (SEC Filings) (2003 10-K page 79).

Its "net value" on "a net present value basis, to settle at current

market rates all outstanding derivative contracts" was (7,712)

million and 8,139 million, which makes a total of 6,633 million

when a "purchased options time value" of 8,139 million is added.

What Fannie

Mae doesn't want is for example a wide "duration gap" for a

long period. If rates turn the opposite way on a duration gap

the cash flow from assets and liabilities may not match, resulting

in inability to pay the bills on liabilities. It reports the

duration gap regularly in its (8-K Regulation FD Disclosure),

see earlier 10-K's for charts and more information (Investor

Relations: Annual Reports & Proxy Statements). (Dec 1999

- Dec 2002 duration gap), (2003 gap).

Speculation

Interest

rate swaps are also used speculatively by hedge funds or other

investors who expect a change in interest rates or the relationships

between them. Traditionally, fixed income investors who expected

rates to fall would purchase cash bonds, whose value increased

as rates fell. Today, investors with a similar view could enter

a floating-for-fixed interest rate swap; as rates fall, investors

would pay a lower floating rate in exchange for the same fixed

rate.

Interest

rate swaps are also very popular due to the arbitrage opportunities

they provide. Due to varying levels of creditworthiness in companies,

there is often a positive quality spread differential which

allows both parties to benefit from an interest rate swap.

The interest

rate swap market is closely linked to the Eurodollar futures

market which trades at the Chicago Mercantile Exchange.

Valuation

and pricing

The present

value of a plain vanilla (i.e. fixed rate for floating rate)

swap can easily be computed using standard methods of determining

the present value (PV) of the fixed leg and the floating leg.

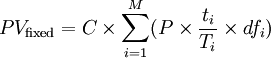

The value

of the fixed leg is given by the present value of the fixed

coupon payments known at the start of the swap, i.e.

where C

is the swap rate, M is the number of fixed payments,

P is the notional amount, ti

is the number of days in period i, Ti

is the basis according to the day count convention and dfi

is the discount factor.

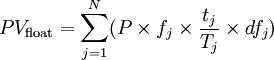

Similarly,

the value of the floating leg is given by the present value

of the floating coupon payments determined at the agreed dates

of each payment. However, at the start of the swap, only the

actual payment rates of the fixed leg are known in the future,

whereas the forward rates (derived from the yield curve) are

used to approximate the floating rates. Each variable rate payment

is calculated based on the forward rate for each respective

payment date. Using these interest rates leads to a series of

cash flows. Each cash flow is discounted by the zero-coupon

rate for the date of the payment; this is also sourced from

the yield curve data available from the market. Zero-coupon

rates are used because these rates are for bonds which pay only

one cash flow. The interest rate swap is therefore treated like

a series of zero-coupon bonds. Thus, the value of the floating

leg is given by the following:

where N

is the number of floating payments, fj

is the forward rate, P is the notional amount, tj

is the number of days in period j, Tj

is the basis according to the day count convention and dfj

is the discount factor. The discount factor always starts with

1. The discount factor is found as follows:

- [Discount

factor in the previous period]/[1 + (Forward rate of the floating

underlying asset in the previous period Ă— Number of days

in period/360)].

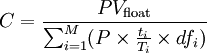

The fixed

rate offered in the swap is the rate which values the fixed

rates payments at the same PV as the variable rate payments

using today's forward rates, i.e.:

[2]

[2]

Therefore,

at the time the contract is entered into, there is no advantage

to either party, i.e.,

Thus, the

swap requires no upfront payment from either party.

During the

life of the swap, the same valuation technique is used, but

since, over time, the forward rates change, the PV of the variable-rate

part of the swap will deviate from the unchangeable fixed-rate

side of the swap. Therefore, the swap will be an asset to one

party and a liability to the other. The way these changes in

value are reported is the subject of IAS 39 for jurisdictions

following IFRS, and FAS 133 for U.S. GAAP. Swaps are marked

to market by debt security traders to visualize their inventory

at a certain time.

Risks

Interest

rate swaps expose users to interest rate risk and credit risk.

- Interest

rate risk originates from changes in the floating rate. In

a plain vanilla fixed-for-floating swap, the party who pays

the floating rate benefits when rates fall. (Note that the

party that pays floating has an interest rate exposure analogous

to a long bond position.)

- Credit

risk on the swap comes into play if the swap is in the money

or not. If one of the parties is in the money, then that party

faces credit risk of possible default by another party. This

is true for all swaps where there is no exchange of principal.

Market

size

The Bank

for International Settlements reports that interest rate swaps

are the largest component of the global OTC derivative market.

The notional amount outstanding as of December 2006 in OTC interest

rate swaps was $229.8 trillion, up $60.7 trillion (35.9%) from

December 2005. These contracts account for 55.4% of the entire

$415 trillion OTC derivative market. However, interest rate

swaps are not standardized enough to allow them to be traded

through a futures exchange like an option or a futures contract.

References

- "Interest Rate Swap" by Fiona Maclachlan, The Wolfram

Demonstrations Project.

- Understanding interest rate swap math & pricing. California

Debt and Investment Advisory Commission (2007-01). Retrieved

on 2007-09-27.

- Pricing

and Hedging Swaps, Miron P. & Swannell P., Euromoney books

1991

External

links