A

currency future, also FX future or foreign exchange

future, is a futures contract to exchange one currency for

another at a specified date in the future at a price (exchange

rate) that is fixed on the purchase date. Typically, one of the

currencies is the US dollar. The price of a future is then

in terms of US dollars per unit of other currency. This can be

different from the standard way of quoting in the spot foreign

exchange markets. The trade unit of each contract is then

a certain amount of other currency, for instance €125,000. Most

contracts have physical delivery, so for those held at the end

of the last trading day, actual payments are made in each currency.

However, most contracts are closed out before that. Investors

can close out the contract at any time prior to the contract's

delivery date.

History

Currency

futures were first created at the Chicago Mercantile Exchange

(CME) in 1972, less than one year after the system of fixed

exchange rates was abandoned along with the gold standard. Some

commodity traders at the CME did not have access to the inter-bank

exchange markets in the early 1970s, when they believed that

significant changes were about to take place in the currency

market. They established the International Monetary Market (IMM)

and launched trading in seven currency futures on May 16, 1972.

Today, the IMM is a division of CME. In the second quarter of

2005, an average of 332,000 contracts with a notional value

of $43 billion were traded every day. Currently most

of these are traded electronically [1].

Other futures

exchanges that trade currency futures are Euronext.liffe [2]

and Tokyo Financial Exchange [3]

The IMM

dates are the third Wednesday in March, June, September and

December.

Pricing

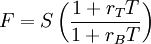

-

The pricing

of a currency futures contract is completely determined by the

prevailing spot rate and interest rates. Otherwise, investors

would be able to arbitrage the difference between the futures

and spot prices.

The futures

price is given by:

where:

- F = futures

price

- S = spot

price

- rT

= interest rate of the term currency

- rB

= interest rate of the base currency

- T = tenor

(calculated according to the appropriate day count convention)

Uses

Hedging

Investors

use these futures contracts to hedge against foreign exchange

risk. If an investor will receive a cashflow denominated in

a foreign currency on some future date, that investor can lock

in the current exchange rate by entering into an offsetting

currency futures position that expires on the date of the cashflow.

For example,

Jane is a US-based investor who will receive €1,000,000 on

December 1. The current exchange rate implied by the futures

is $1.2/€. She can lock in this exchange rate by selling €1,000,000

worth of futures contracts expiring on December 1. That way,

she is guaranteed an exchange rate of $1.2/€ regardless of

exchange rate fluctuations in the meantime.

Speculation

Currency

futures can also be used to speculate and, by incurring a risk,

attempt to profit from rising or falling exchange rates.

For example,

Peter buys 10 September CME Euro FX Futures, at $1.2713/€.

At the end of the day, the futures close at $1.2784/€. The

change in price is $0.0071/€. As each contract is over €125,000,

and he has 10 contracts, his profit is $8,875. As with any future,

this is paid to him immediately. Edit: Quoting for FX Futures

at CME is in €/$ not $/€!

More generally,

each change of $0.0001/€ (the minimum Commodity tick size),

is a profit or loss of $12.50 per contract.}}